What Einhorn Didn’t Mention About Core

A few things that Einhorn didn't mention in his presentation, but surely must have caught his interest.

Introduction

In recent years David Einhorn’s Greenlight Capital, has struggled despite a rising market. Short positions on Amazon and Tesla have hurt performance, leading to single-digit, under-performing returns. Still, Einhorn is well-regarded for detailed analysis such as his short of Allied Capital (documented in his book Fooling Some of the People All of the Time) and a prescient, public statement against Lehman Brothers.

In his latest public short, Einhorn continues on the theme raised in his 2015 presentation criticizing of oil companies by presenting a compelling short thesis on Core Laboratories (“Core”; CLB).

Core at a Glance

History

Core was founded in 1936, in Houston, Texas. During the next sixty years, it would be publicly offered and acquired by Litton, then ultimately spun-off in 1994 to form Core Laboratories as it’s known today. When it was spun-off, a group from its management agreed to buy it. Since then, David Demshur has been Core’s CEO. The company is now dual-listed on the Euronext and headquartered in Amsterdam.

Core Business

Core provides technology that helps oil companies extract more efficiently. That being said, their revenues are tightly linked to the R&D spending of oil companies and ultimately, to the price of oil. After their revenues weathered the 2009 fall in oil prices, analysts declared Core to be secular and have since given them a higher premium and rosier expectations. Roughly stated, Einhorn believes Core has built marketing hype surrounding non-oil energy sources while employing buybacks, stock issuance, and dividend nonsensically. At the same time, analysts have overlooked the cyclical, oil-dependent nature of their earnings.

The Secular Misnomer

Core’s business proposition is simple. They help their clients (e.g. British Petroleum, Saudi Aramco, Exxon) recover more oil and increase their return-on-investment (ROI). The ROI for these companies is heavily impacted by shifting energy prices. Higher prices mean greater revenues.

Analysts gave Core the ‘secular’ label in 2009 after its revenues appeared relatively immune to the 2008 decline in oil prices. Secular companies get higher premiums because they’re not subject to cyclical risks such as fluctuating energy prices. Despite lower oil prices in 2008-2009, Core’s customers maintained their capital expenditures and investment – resulting in the ‘secular’ label.

Since the 2015 oil slump, declining oil prices have been met by decreased Global CapEx. As cited by Einhorn, Halliburton and Schlumberger both mention that they’re focusing their CapEx in North America. Global is much more profitable for Core than North America, and so unlike 2009, the current decline demonstrates that Core is much more cyclical than previously thought.

What’s more interesting, in multiple interviews, Core’s CEO is often heard speculating about a “V-shaped recovery.” A skeptic would imagine that CEO’s don’t repeat themselves without a reason. His repeated speculations suggest that the anticipation of higher oil prices would benefit Core’s business.

Mixed Up Metrics

“Core is a non-capital intensive business. Analytically, the ROIC in a non-capital intensive business is irrelevant, because you can’t reinvest your profits to grow your earnings at the stated ROIC. Core could have twice as much lab equipment without gaining any new customers. It is flawed to value the stock based on its ‘industry leading ROIC.’” - Einhorn at Ira Sohn, 2017

Core is largely heralded for their high return on invested capital (ROIC) despite, according to Greenlight Capital, not being a capital-intensive business. Capital-intensive business are unable to scale without additional capital investments. For example, to increase revenues, an airliner has to scale up their fleet of planes. Core’s customers, the oil-producers, have to invest in equipment in order to increase capacity. Core, on the other hand, expands its offerings via research and development.

The Dividend Shuffle: Robbing Peter to Pay Peter

Despite declining revenues, Core has paid out dividends larger than their earnings for the last five quarters. Bizarrely, the shortfall was being funded by issuing stock. Shareholders were receiving dividend payments that were funded by diluting the value of their shares held.

Add to this, a run of consistent debt-funded buybacks that nearly triggered a debt covenant related to their EBITDA. For the cherry on top, we can’t overlook this great Einhorn snark-quote:

“When a company raises fresh money from new investors to sustain the income requirements of existing investors, there’s a name for that.” 2017 Ira Sohn presentation, Slide #63

It’s nowhere as direct as “the Motherfracker” label he applied to Pioneer Natural Resources, but it’s much more barbed. Clearly, this quote alludes to a Ponzi scheme. A Ponzi scheme creates the image of a lucrative investment by repaying early investors with investments from new investors. Among Einhorn’s criticisms of Core, this stood out to me as being particularly pointed.

What Wasn’t Mentioned

Core’s CEO, David Demsur, plays a significant role in Einhorn’s presentation. In researching a bit on Core, I found two things that Einhorn didn’t mention in his presentation, but that I’m sure must have gotten his interest.

“Mr. Demshur serves as the Company’s Chief Executive Officer and as Chairman of the Supervisory Board (“Chairman of the Board”). Given the size of the Company, we believe our shareholders are well served by having Mr. Demshur hold the Chief Executive Officer role along with being Chairman of the Board and that this is the most effective leadership structure for us at the present time. We also note that within our industry, the common practice is for the same person to hold both positions. We believe this structure has served us well for many years.” From Core’s March 2017 DEF-14A

Demshur holds positions as President, CEO, and Chairman. While a CEO/President can raise concerns about separation of powers and oversight, Core claims that Demshur isn’t involved in meetings regarding his own compensation.

“Our CEO provides recommendations to the Compensation Committee in its evaluation of our NEOs, including recommendations of individual cash and equity compensation levels for each of the NEOs…Mr. Demshur does not participate in discussions regarding his own pay.”

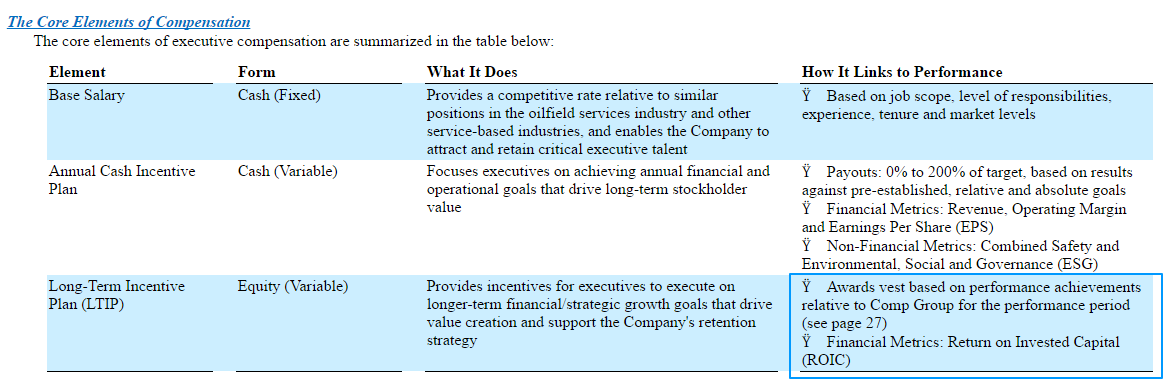

Demshur’s compensation is an interesting matter – 73% comes from the Long Term Incentive Plan, which is tied to Core’s return on invested capital relative to peer companies.

This begs the question:

if, as Einhorn suggests, ROIC is an irrelevant metric for Core Laboratories, then why is it the determining factor in their executive compensation?

Closing

As a reasonable valuation, Einhorn suggests the stock price is nearly cut in half to $62. This reflects an anticipated average earnings of 3.50/share at a P/E ratio of 17.7x.

It remains to be seen if and when Einhorn’s thesis comes to fruition. Einhorn’s a poker player – maybe he hasn’t shown his full hand yet. What is certainly made clear by a presentation illustrated with clergy, chameleons, and Kanye – someone at Greenlight has pretty solid sense of humor.

-Arsene